Aeon Balanced Prescient Fund

Investment Philosophy

The Aeon Balanced Prescient Fund aims to provide clients with a 90% downside capital protection over a rolling 12-month period and attempts to remove emotions of investing. It utilizes a systematic return modelling process and a disciplined investment methodology. The balanced fund strategy recognizes that equities have more upside potential than fixed income and over the long term, equities have proved to be a superior inflation hedge. There is also increasing long term uncertainty of bond risk given global monetary and fiscal expansion.

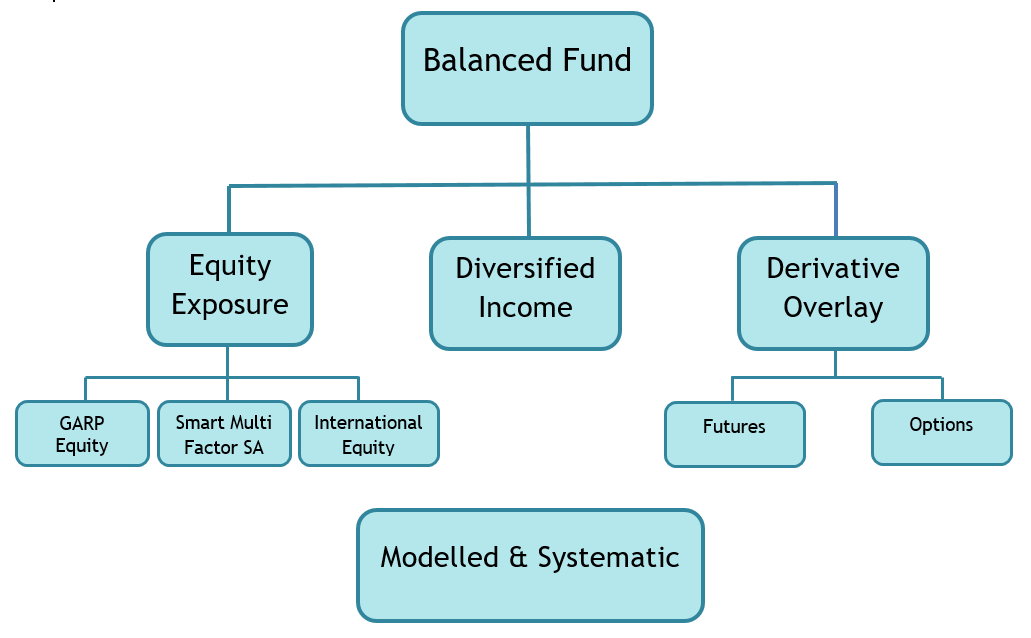

Equity stock universe long positions are based on Growth At Reasonable Price. Significant inefficiencies can occur in equity valuations due to market participants having excessive optimism or pessimism regarding the outlook for the market or individual companies. The over-allocation of capital to a certain investment style (growth or value) can also lead to inefficiencies in the market price of securities. We look to capitalize on these inefficiencies by buying companies with long term sustainable growth rates greater than that implied by the company’s market valuation. We also utilise our in-house currency model and Fear & Greed Index for foreign asset allocation. Aeon Balanced Prescient Fund’s investment strategy encompasses active asset allocation and active management of underlying equity and fixed income assets. Derivatives are used to protect all risky assets.

Investors should consider the Aeon Balanced Prescient Fund where they have a long term horizon (3 years or longer), and are looking for capital growth with foreign equity exposure.

Investment Objectives

Aeon’s Balanced Fund strategy invests in a range of income, domestic and foreign equity assets and strategies in order to:

- Earn inflation-beating returns by investing in the full spectrum of domestic and foreign equity and fixed income markets.

- Provide investors with stable income and modest capital appreciation in the long run.

- Manage risk through disciplined portfolio construction.

- Employ low cost trading techniques.

Risk Management and Return Modelling

The portfolio is structured with overweight and underweight positions relative to the benchmark, which is dependent on the gap between the implied and sustainable growth rates. A real time model monitors the portfolio positions, and the effect of the sector and stock selection decisions on the performance relative to benchmark. The risk management framework encourages diversification and reduces the risk of significantly underperforming the benchmark.

Strategy Benefits

Portfolio returns are modelled in a range of market scenarios to ensure maximum possible upside is captured while maintaining downside protection.

A consistent implementation of our philosophy is expected to lead to outperformance of the benchmark (CPI +5%) in the long run, regardless of the dominant investment style.

Disclaimer

Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. CIS’s are traded at the ruling price and can engage in scrip lending and borrowing. A schedule of fees, charges and maximum commissions is available on request from the Manager. There is no guarantee in respect of capital or returns in a portfolio. A CIS may be closed to new investors in order for it to be managed more efficiently in accordance with its mandate. Performance has been calculated using net NAV to NAV numbers with income reinvested. A detailed disclaimer can be viewed here.

“Man can believe the impossible, but man can never believe the improbable.” – Oscar Wilde